How Falling Behind on Bookkeeping Hurts Cash Flow

Introduction

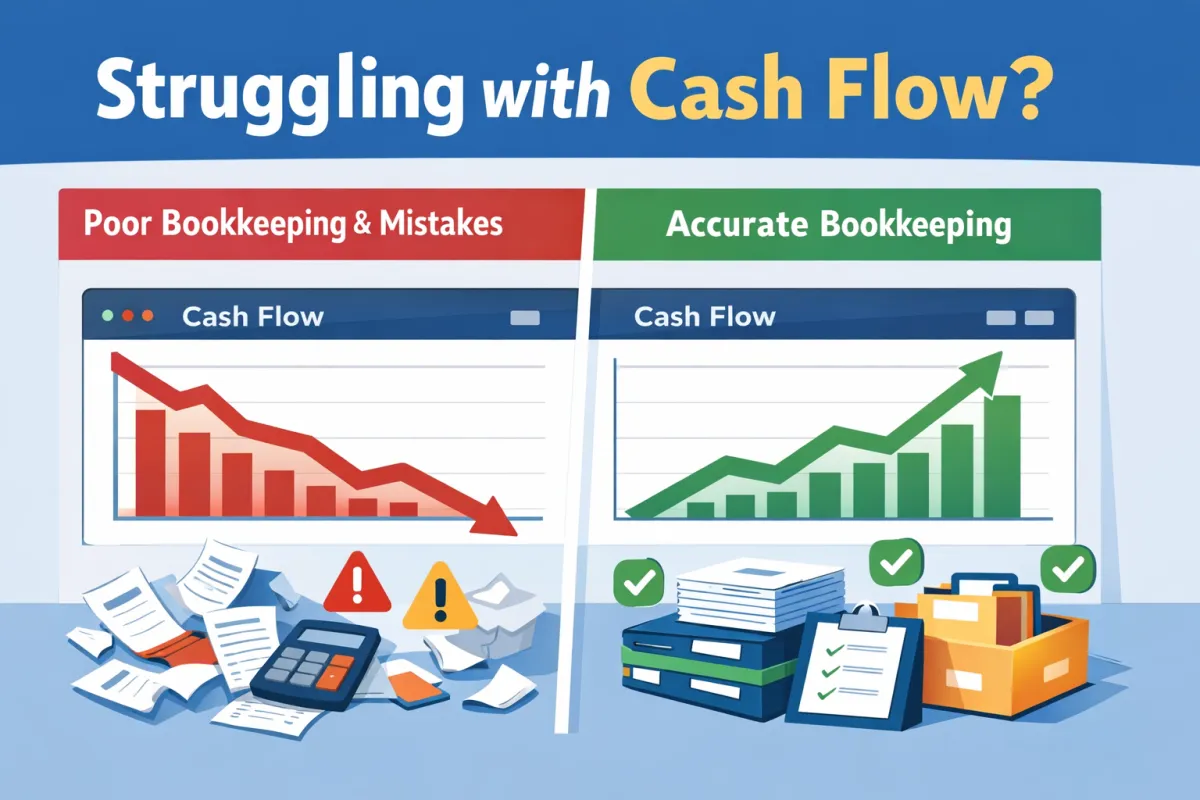

Bookkeeping is the backbone of every small business, playing a pivotal role in financial health. When businesses delay or neglect their bookkeeping responsibilities, they can experience significant cash flow challenges. Poor bookkeeping practices might seem minor at first glance, but they can lead to cash shortages and financial instability if not addressed. Common mistakes—such as disorganized records or misclassifying transactions—often go unnoticed, further exacerbating cash flow issues.

The Link Between Bookkeeping & Cash Flow

Timely and precise bookkeeping is essential for maintaining healthy cash flow. Accurate records allow businesses to forecast revenue, budget expenses, and plan for growth. When bookkeeping is neglected, the resulting errors can create significant cash flow problems, such as unexpected shortfalls during critical periods. For instance, failing to record incoming payments promptly can lead to a misrepresentation of available cash, causing unnecessary stress and operational delays.

Common Bookkeeping Mistakes That Hurt Small Businesses

Small businesses often fall victim to various bookkeeping mistakes that can have severe repercussions:

Misclassifying income and expenses: This can lead to inaccurate financial reports and misguided financial decisions.

Mixing personal and business transactions: This blurs the lines in financial reporting, complicating tax preparation and potentially leading to audits.

Forgetting to record small or recurring transactions: Even minor transactions add up over time, and omitting them can significantly skew cash flow analysis.

Inconsistent reconciliation of bank and credit card accounts: Failing to regularly reconcile these accounts can result in missed discrepancies and unknown liabilities.

How Poor Bookkeeping Leads to Costly Consequences

Neglecting proper bookkeeping can lead to several costly consequences, including:

Cash flow shortages: Suddenly facing unexpected financial gaps can disrupt day-to-day operations and impede growth.

Tax complications: Inaccurate records can result in overpaying or underpaying taxes, leading to penalties and interest charges.

IRS red flags or audits: Poor documentation can trigger audits, causing stress and potential financial penalties from the IRS.

Missed deductions: Failing to record eligible expenses can result in higher tax liabilities.

Vendor payment delays: Late payments can strain relationships with suppliers, potentially jeopardizing future collaborations.

Warning Signs Your Bookkeeping Is Falling Behind

It's crucial to be aware of the warning signs indicating that bookkeeping may be faltering:

Incomplete or outdated records: Difficulty locating crucial documents can indicate neglected bookkeeping.

Constantly guessing your actual cash position: Uncertainty about cash flow suggests gaps in financial tracking.

Unexplained discrepancies in accounts: Regular inconsistencies can signal serious data entry errors or fraud.

Difficulty preparing financial statements: If producing financial reports becomes a challenge, it may indicate inadequate recordkeeping.

Best Bookkeeping Practices to Avoid Costly Mistakes

To maintain a robust financial framework, small businesses should adopt best bookkeeping practices, such as:

Prioritizing regular reconciliation: Consistent reconciliation of accounts ensures accuracy and identifies errors promptly.

Keeping receipts and documentation organized: Organized records facilitate easier auditing and tax preparation.

Implementing a clear chart of accounts: A structured chart of accounts simplifies tracking and reporting.

Using bookkeeping software to automate tasks: Automation minimizes manual errors and streamlines processes.

Doing monthly reviews: Regular financial reviews can help catch mistakes before they escalate into significant issues.

When to Hire a Professional Bookkeeper

Recognizing when to hire a professional bookkeeper is vital for safeguarding your business's cash flow. Signs that it may be time to seek expert help include:

Feeling overwhelmed by bookkeeping tasks or realizing you've fallen behind.

Understanding that a professional can help mitigate audit risks and costly errors.

A financial expert can also provide guidance on optimizing cash flow and maintaining compliance with tax laws.

Keeping your bookkeeping in check is a fundamental part of ensuring your small business thrives. By avoiding common mistakes, recognizing the importance of timely financial tracking, and employing best practices, you can protect your cash flow and contribute to the long-term success of your enterprise.